Summary

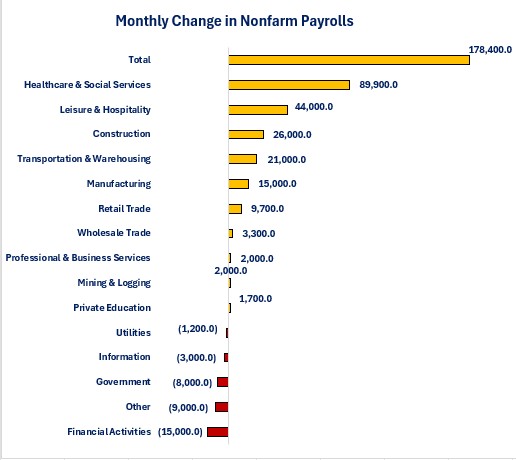

Jobs growth rebounded in the US in March. The nation added 178,000 jobs in March which far exceeded the median forecast of economists surveyed by Bloomberg. Their forecast was for 70,000 jobs to be added.

The results also broke the streak of previous month's data being revised lower. February's job growth was revised higher by 34,000. January was revised lower by 44,000. The Health Care & Social Services industry continues to dominate jobs growth as it accounted for just over 50% of total net jobs growth.

The Unemployment rate fell from 4.4% to 4.3% and the Labor Force Participation Rate fell from 62.0% to 61.9%. From an income standpoint, employees were happy as total average weekly earnings rose faster than the official inflation rate. The year-over-year growth was 3.5%.

Establishment Survey

Health Care & Social Services accounted for 50.4% of total net jobs growth and when you add in the 44,000 jobs added by Leisure & Hospitality, the top two industries accounted for 75.1% of total net jobs growth. Five industries lost jobs while ten industries added jobs.

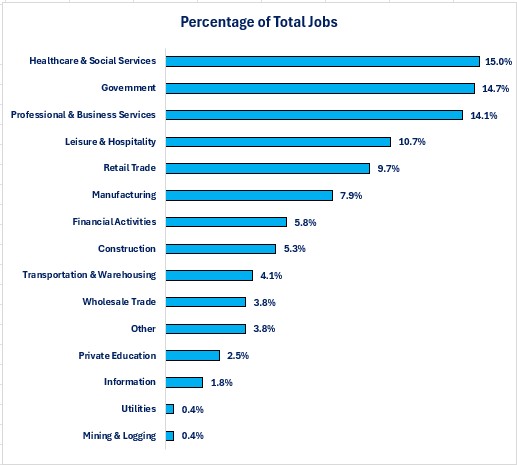

When examining the percentage of total jobs that each industry comprises, Health Care & Social Services is the leader as it makes up 15.0% of total jobs.

Government is second at 14.7% and Professional & Business Services is third at 14.1%. These three industries make up 43.8% of total jobs.

The Mining & Logging and Utilities industries make up the smallest percentages at 0.4% each.

From an income perspective, even though total average weekly earnings rose 3.5% year-over year, there was a wide dispersion of growth rates among industries.

The Utilities industry had the highest year-over-year growth at 6.6% while the Education & Health Services sector experienced the lowest growth at 1.8%.

That is a problem since the Utilities industries lost jobs and the Education & Health Services industry added the most jobs.

The picture is even more stark when you consider the actual dollar growth by industry. Total average weekly earnings rose $43.44 on a year-over-year basis but employees in the Utilities sector saw their average weekly earnings rise $145.54 while employees in the Education & Healthcare sector received a $19.23 increase.

Examining total average weekly earnings by industry highlights the bifurcation between the higher paying industries and lower paying industries.

As you can see from the graph below, the two industries with the most jobs added in March are in the bottom four for wages.

Household survey

The Household Survey showed far different results than the Establishment Survey. As discussed in previous updates, this is not unusual on a month-by-month basis but tends to even out over time.

The Household Survey showed the number of people employed (not jobs created) fell by 64,000 and the number of unemployed people fell by 332,000. As a result, the official unemployment rate fell from 4.4% to 4.3%. The labor force fell 396,000.

This resulted in the labor force participation rate falling from 62.0% to 61.9%. Multiple job holders fell by 14,000, but the percentage of employed people who are working multiple jobs remained at 5.1% of total employment.

For those who were already unemployed the data showed improvement. The average duration of unemployment fell from 25.7 weeks to 25.3 weeks. Before we get too excited, we must consider that this may be because people who were previously unemployed stopped looking for work.

With the labor force declining 396,000 and the number of unemployed declining 332,000, that indicates that many of the previously unemployed people may have stopped looking for work.

If you are not actively looking for work, you are no longer part of the labor force and you are no longer classified as unemployed. The percentage of people who have been unemployed 27 weeks or more rose from 25.3% to 25.4%.

Conclusions

-

March's results are encouraging given the steady decline in jobs being added over the last year.

-

It is also encouraging that February's results were revised up rather than down. One month does not establish a trend but it is still encouraging.

-

The concentration of jobs growth in a few industries remains a risk for the economy if anything negative happens in these industries.

-

From a financial health standpoint, it is concerning that the industries that are creating the most jobs are also at or near the bottom of the salary scale. These employees may find themselves in financial distress since their wages may not be sufficient to cover the major expenses like rent, daycare, and insurance.

-

March's results will most likely reinforce the Federal Reserve's “wait and see” position for interest rates and will probably keep it from lowering short-term interest rates in the near term.

Steve is the Economist for Washington Trust Bank and holds a Chartered Financial Analyst® designation with over 40 years of economic and financial markets experience.

Throughout the Pacific Northwest, Steve is a well-known speaker on the economic conditions and the world financial markets. He also actively participates on committees within the bank to help design strategies and policies related to bank-owned investments.