Summary

After experiencing jobs growth over 100,000 for four out of the first five months of the year, jobs growth sank below 100,000 in June. The Bureau of Labor Statistics (BLS) reported a 57,200 increase in jobs in June. The Healthcare & Social Services industries dominated the net jobs growth with 46,600 jobs added. The Leisure & Hospitality industry was the primary reason for jobs growth being below 100,000 as this industry lost 61,000 jobs. Average weekly earnings rose 3.8% on a year-over-year basis and the unemployment rate fell from 4.3% to 4.2% due to a decline in the labor force. June's employment data will support the case for those Federal Reserve members who want to hold the overnight borrowing rate unchanged versus those who were leaning toward raising the rate.

Establishment Survey

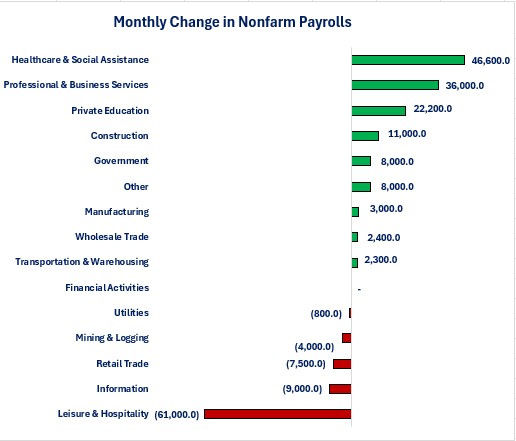

The Healthcare & Social Assistance industry led the way with 46,600 jobs added in June. Within that industry, the Social Assistance sub-industry added the most jobs with 25,100 jobs added. Nine industries added jobs while five industries lost jobs and one industry (Financial Activities) was unchanged. The Leisure & Hospitality industry suffered the biggest job losses with 61,000 jobs lost. Within the industry, the Food Services & Drinking Places sub-industry suffered the most job losses with 32,900 jobs lost.

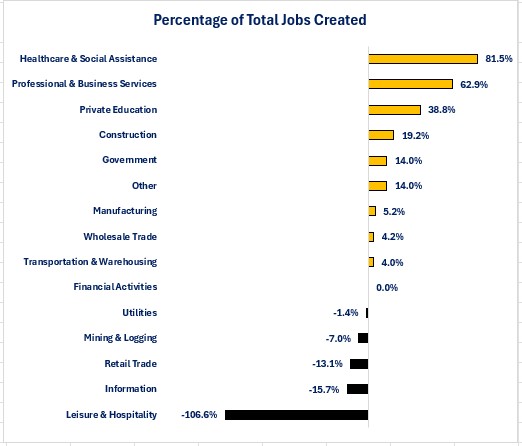

On a net jobs creation basis (i.e., jobs added minus jobs lost), the Healthcare & Social Assistance industry accounted for 81.5% of net jobs created. As you can see from the chart below, the Leisure & Hospitality industry lost more jobs than the total 57,200 net jobs created. Strength in jobs additions within the Professional & Business Services and Private Education helped offset the large losses in the Leisure & Hospitality industry.

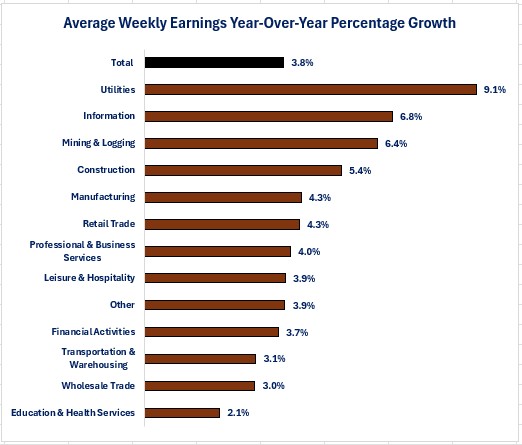

From an income standpoint, average weekly earnings grew 3.8% on a year-over-year basis. The Utilities industry experienced the biggest growth in wages while the industry that added the most jobs-Education & Health Services-experienced the smallest increase.

Household survey

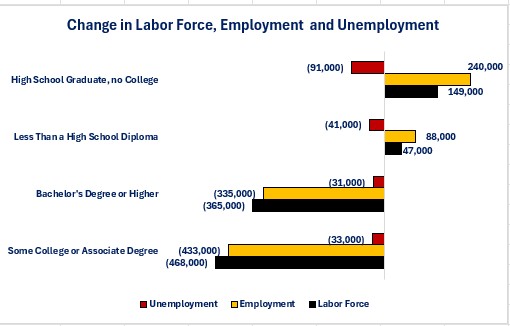

The Household Survey showed a 507,000 decrease in the number of people reporting they were employed. The survey also showed a 213,000 decrease in the number of people reporting they were unemployed. This resulted in a 720,000 decrease in the labor force. That translated into the unemployment rate declining from 4.3% to 4.2%, but the labor force participation rate declined from 61.8% to 61.5%.

If we examine the three components (unemployment, employment, and labor force) by educational attainment we learn that all educational categories experienced a decrease in the number of people reporting they were unemployed. The story is different for the number of people reporting they were employed. The two lowest educational attainment categories reported increases in employment, but those gains were offset by large decreases from the upper two educational attainment categories. There have been numerous reports of the struggles of college graduates unable to find work, and the graph below supports those reports.

The number of people working multiple jobs rose by 126,000 in June and the percentage of multiple job holders as a percentage of total employed rose from 5.2% to 5.3%. For those already unemployed, the average duration of unemployment fell from 26.0 weeks to 25.5 weeks. The percentage of people who have been unemployed for 27 weeks or more fell from 27.5% to 27.3%. What the data does not tell us is whether this is due to people giving up looking for work and thus, no longer counted as unemployed.

Conclusions

-

Although weaker than forecast, the nation still added jobs in June, but at a slower pace than the previous months of the year.

-

More industries added jobs than reduced jobs, but net jobs growth remains concentrated in a few industries.

-

The slower pace of jobs growth supports those Federal Reserve members who want to continue to hold the overnight borrowing rate unchanged versus those who indicated that increasing interest rates may be in order.

Steve is the Economist for Washington Trust Bank and holds a Chartered Financial Analyst® designation with over 40 years of economic and financial markets experience.

Throughout the Pacific Northwest, Steve is a well-known speaker on the economic conditions and the world financial markets. He also actively participates on committees within the bank to help design strategies and policies related to bank-owned investments.